For many years, ESG reporting looked like a branding exercise. Companies published sustainability brochures filled with aspirations, but with little consistency or accountability. That approach no longer works.

Across both developed and emerging economies, ESG reporting is becoming structured, comparable, and increasingly regulated. What we are seeing today is not one single standard, but a global ESG reporting system made up of interconnected frameworks — each answering a different question.

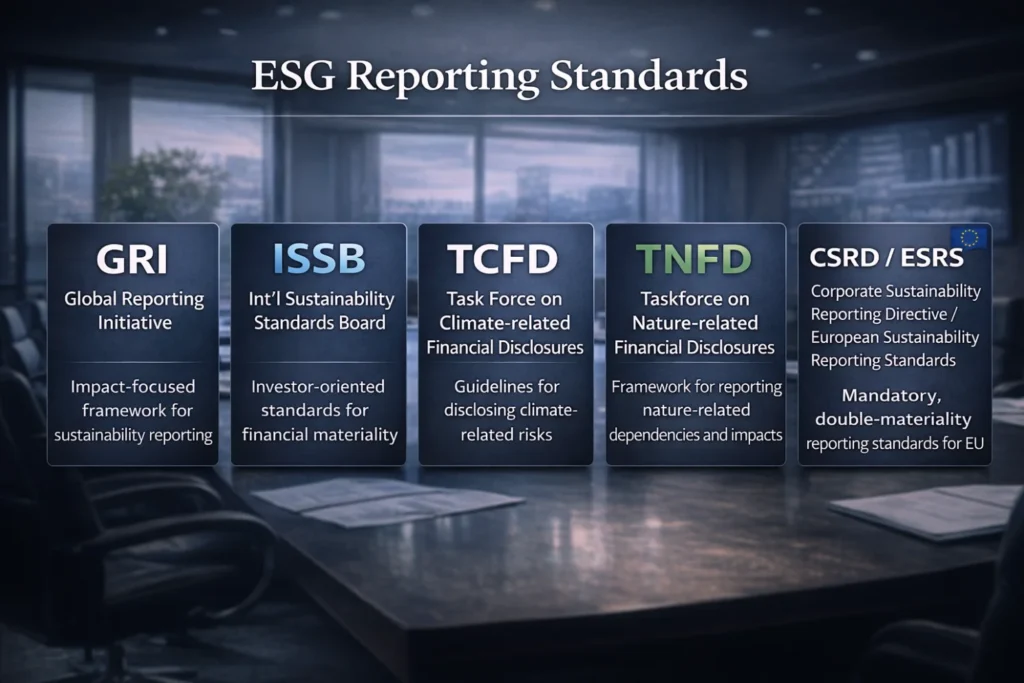

1. Impact Comes First: GRI and the Global South

The modern ESG journey begins with impact.

The Global Reporting Initiative (GRI) introduced the idea that companies must disclose how their operations affect people, communities, and the environment, not just profits. This approach — known as impact materiality — has been especially influential in the Global South, where social and environmental impacts are often more visible and more immediate.

Examples:

- India: Many listed companies historically used GRI-based sustainability reporting, which later informed India’s mandatory Business Responsibility and Sustainability Reporting (BRSR) framework.

- South Africa: Companies commonly align GRI disclosures with King IV governance principles, especially around workforce equity, community impacts, and social transformation.

For organizations operating in emerging markets, GRI often serves as the most practical starting point, because it captures impacts that regulators, communities, and global buyers actually care about.

2. Investor Lens: ISSB as a Complement, Not a Replacement

As global capital flows into emerging markets, investors began asking a different question: Which sustainability issues could affect enterprise value?

This led to the creation of the International Sustainability Standards Board (ISSB) under the IFRS Foundation. ISSB’s standards — IFRS S1 and IFRS S2 — focus on financial materiality, meaning sustainability risks and opportunities that may affect financial performance.

Important clarification: ISSB adoption varies by jurisdiction. Some countries are mandating or formally adopting ISSB standards, while others reference them as guidance or use them voluntarily — particularly for investor-facing disclosures.

Examples:

- Brazil: Companies issuing green or sustainability-linked bonds increasingly align climate risk disclosures with ISSB expectations to meet international investor demands.

- Southeast Asia: Jurisdictions such as Singapore are explicitly aligning sustainability reporting regimes with ISSB as a baseline.

From a GRI-first strategy, ISSB works best as a second layer — translating real-world impacts into investor-relevant financial risk where required.

3. Climate as the Gateway: TCFD

Climate reporting became mainstream through the Task Force on Climate-related Financial Disclosures (TCFD), which structured disclosures around governance, strategy, risk management, and metrics.

Examples:

- Chile: Mining companies used TCFD-style reporting to explain exposure to water stress and transition risks.

- Global supply chains: Multinationals increasingly require TCFD-aligned disclosures from suppliers operating in Africa, Latin America, and Asia.

Today, TCFD lives on inside ISSB IFRS S2, reinforcing climate as the entry point to more comprehensive ESG reporting.

4. Regulation Raises the Bar: CSRD and ESRS

Europe fundamentally changed ESG reporting through the Corporate Sustainability Reporting Directive (CSRD) and the European Sustainability Reporting Standards (ESRS).

The EU mandates double materiality, requiring disclosure of:

- Financial risks to the company

- Impacts on society and the environment

Why this matters for the Global South:

- Non-EU companies with significant EU operations must comply.

- Export-oriented firms in Bangladesh, Vietnam, Morocco, and Africa face rising ESG data demands because European buyers must now report across their value chains.

For GRI reporters, ESRS does not replace existing work — it builds directly on impact-based disclosures, formalizing and assuring them.

5. Beyond Climate: Nature and TNFD

Climate alone does not capture environmental risk.

The Taskforce on Nature-related Financial Disclosures (TNFD) addresses biodiversity, water, land use, and ecosystem dependencies using the LEAP () approach.

Examples:

- Brazilian agribusiness: Mapping deforestation and water risks to maintain market access.

- South Asian agriculture and textiles: Responding to growing scrutiny on water stress and land impacts.

TNFD naturally complements GRI environmental disclosures, deepening nature-related impact analysis where risks are material.

6. Data at Scale: CDP and Market Pressure

CDP operates as a disclosure platform, collecting standardized climate, water, and forest data.

Examples:

- Many companies in India, China, and Africa disclose through CDP because multinational customers and lenders request it — even without domestic mandates.

CDP reinforces transparency and comparability but does not replace standards.

7. Interoperability: A GRI-First System That Scales

The strongest reporting architectures today follow a GRI-first strategy:

- Start with GRI to identify and disclose real-world impacts

- Translate material impacts into financial risk using ISSB where required

- Align with ESRS for EU compliance

- Extend into TNFD for nature-related risks

This enables “report once, use many times” — especially critical for companies in emerging markets with limited reporting resources.

Conclusion: ESG Reporting Is Now A Critical Infrastructure

ESG reporting is no longer about narratives. It is about systems, governance, data, and assurance.

For companies in the Global South, a GRI-first approach remains the most grounded and credible foundation — because it starts with impacts on people and the environment, then scales upward to meet investor and regulatory expectations. Ultimately, what we now see is a set of Global ESG Reporting Systems — interconnected, interoperable, and unavoidable.

The question is no longer whether to report, but how well your reporting system reflects reality.

References (Selected, Publicly Available)

- Global Reporting Initiative (GRI) – GRI Standards and Impact Materiality

- IFRS Foundation – ISSB IFRS S1 & S2 Sustainability Disclosure Standards

- Task Force on Climate-related Financial Disclosures (TCFD) – Final Recommendations

- European Commission – Corporate Sustainability Reporting Directive (CSRD)

- EFRAG – European Sustainability Reporting Standards (ESRS)

- Taskforce on Nature-related Financial Disclosures (TNFD) – LEAP Approach

- CDP – Climate, Water, and Forests Disclosure Framework

- SEBI (India) – Business Responsibility and Sustainability Reporting (BRSR)

- King IV Institute (South Africa) – King IV Report on Corporate Governance

- Comissão de Valores Mobiliários (Brazil) – CVM ESG Disclosure Guidance